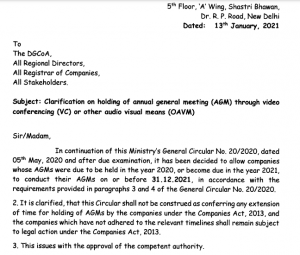

GST registration is required for Charitable Trust running medical store to give medicines without profit. Since charitable Trust is running a medical store, and selling medicines to customers at a lower rate with no profit, sale of medicine by Trust would be a taxable supply of goods; aggregate turnRead more

GST registration is required for Charitable Trust running medical store to give medicines without profit.

Since charitable Trust is running a medical store, and selling medicines to customers at a lower rate with no profit, sale of medicine by Trust would be a taxable supply of goods; aggregate turnover exceeding threshold limit, Trust would have to obtain registration

See less

interest earned on account of funds borrowed for specific purpose shall not be taxed but interest received on investment of surplus funds is taxable in other income. In the matter of HP Power Transmission Corporation Ltd Vs DCIT, ITAT gave order. Assessee company HP Power Transmission Corporation LRead more

interest earned on account of funds borrowed for specific purpose shall not be taxed but interest received on investment of surplus funds is taxable in other income.

In the matter of HP Power Transmission Corporation Ltd Vs DCIT, ITAT gave order.

Assessee company HP Power Transmission Corporation Limited (HPPTCL), a Government undertaking, was yet to start commercial operation. As per details of “Other income”, assessee had earned interest on bank deposit during period relevant to AY. Interest was earned on surplus funds available with assessee company but it was not offered for taxation. AO rejected assessee’s submission in that regard and interest was assessed to tax in hands of assessee as ‘income from other sources”. As CIT (A) upheld AO’s order, assessee filed present appeals. Both AO and CIT (A) had held that issue had been decided against assessee by ITAT in preceding years and facts of relevant AY were not different from preceding AYs.

On Appeal, ITAT held that,

Whether interest earned on account of funds borrowed for specific purpose can be taxed – NO: ITAT.

Regarding interest income earned, the relevant fact was nature and composition of interest income earned, i.e, surplus funds and specific purpose funds and not factum of loan. For earlier AY in assessee’s case, when interest was earned by assessee on surplus funds available with it, issue was decided against assessee. For AY in case of HP Power Corporation, assessee had borrowed certain amount from Asian Development Bank (ADB) for specific project and on account of delay in project, parked the amount in temporary investments in FDRs. Interest earned thereon was held by ITAT to be not taxable. Thus, facts during the year were partly different with funds having been borrowed for specific purpose and parked in FDRs as temporary investments on account of delay in project. Thus, distinction in facts in the aforestated two orders was that while in case of assessee in earlier years, interest was found to be earned on surplus funds and hence held taxable, in case of HP Power corporation, interest was earned on specific purpose funds deposited in FDRs on account of delay in execution of projects and therefore, held not taxable. It was thus held that interest received to extent of ADB loan parked in investments in FDRs was not revenue in nature and not liable to be taxed under the head “income from other sources”.

- ITA No. 789/Chd/2019

- ITA No. 790/Chd/2019

See less